ta’ameen Qatar summarises Alpen Capital’s report on Qatar and presents key pointers for its stupendous growth in the insurance space.

The Past & the Present:

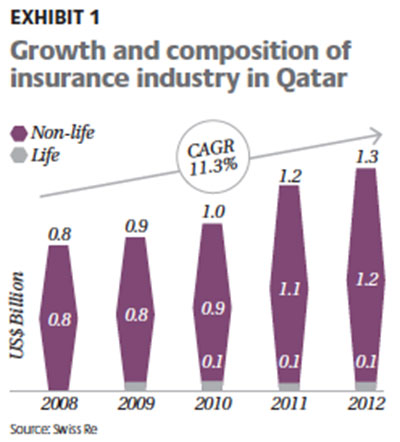

Until 2006, Qatar trailed behind Kuwait in terms of total Gross Written Premium (GWP) in the insurance industry. By 2012, Qatar’s insurance industry was worth USD 1.3 billion and had outperformed its closest GCC counterpart Kuwait and had expanded at an annual average growth rate of 11.3 percent between 2008 and 2012. This industry growth can be attributed to a combined impact of economic progress, substantial focus on infrastructure development, increasing population and compulsory insurance regulations.

Penetration:

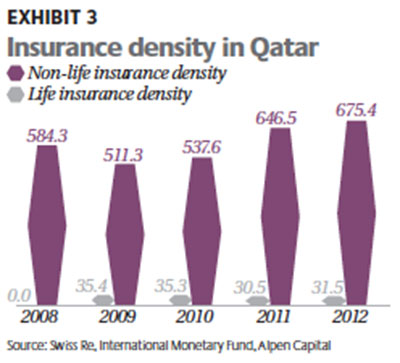

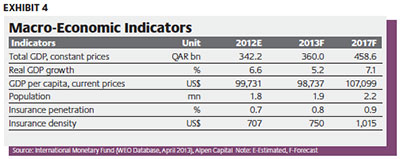

Insurance penetration in Qatar was 0.7 percent in 2012, only slightly above that in Kuwait. Since 2009, it had declined significantly as the overall GDP growth outpaced the rate of expansion of the insurance industry. However, insurance density at USD 706.9 was significantly higher than that of Kuwait.

Insurance density: Life & Non-Life:

The life insurance market has evolved to a perceptible size only since 2009, before which, the non-life segment contributed towards almost the entire insurance premium in the country.

Even as the life insurance market accounted for less than five percent of the total industry in 2012, Qatar stood favourably in terms of overall insurance density as compared to the GCC average due to a sizeable non-life insurance sector. In fact, the country presents a contrasting picture of insurance density between the life and non-life segments at the regional level.

While it had the second-lowest density in the life insurance segment in 2012, it ranked second from the top in non-life insurance density.

Growth drivers:

Demography:

Population in Qatar is expected to expand at 4.0 percent annually between 2012 and 2017, making it the fastest growing resident community in the GCC. A largely expatriate workforce and increasing age profile of residents also bodes well for the insurance sector.

Affluence:

Qatar is one of the wealthiest countries in the world in terms of GDP per capita. High personal wealth and healthy economic growth suggest strong prospects of people and businesses to invest in insurance products.

Construction activities:

Pursuant to its long-term vision and in preparation for the 2022 FIFA World Cup, infrastructure spending in Qatar is projected to reach USD 150 billion. The swift face of construction being undertaken in the country is providing a major boost to the non-life insurance segment.

Health insurance:

Imminent introduction of the compulsory medical insurance law covering nationals, expatriates and visitors is expected to fuel substantial growth of the segment.

Business environment:

The QFC has become a base for international insurance companies due to its favourable business environment. Liberal government policies, ease of doing business and opportunities for underwriting large commercial risks have attracted many primary insurers and reinsurers to the country.

Regulatory Amendments:

Until recently, the Qatari insurance sector was regulated by the insurance law of 1966, which imposed a number of restrictions such as permitting only a national insurer to insure properties within Qatar, restricting foreigners from operating as insurance agents or owning such entities and requiring all Qatari insurance companies to be established as joint stock companies completely owned by nationals.

In December 2012, the Emir of Qatar passed the Law of the Qatar Central Bank and the Regulation of Financial Institutions. Although the new law fell short of creating a single regulator for monitoring all banks, insurance and financial services companies located within the geographical boundaries of Qatar, it paved the way for such a possibility in the future. The law also transferred the responsibility of licensing and supervision of all insurance companies, reinsurance companies and insurance intermediaries from the Ministry of Business and Trade onto Qatar Central Bank.

Qatar Central Bank

Takaful:

QFC has introduced regulations specifically for the Takaful market. In contrast, Qatar (excluding QFC) does not have an explicit rulebook for governing the Takaful operators market yet.

QFC: The financial service hub:

The government had established the Qatar Financial Centre (QFC) in 2005 to boost growth of the financial services industry and foreign investments in the country. By offering an investment friendly environment, the zone provides a conduit to foreign insurance companies for establishing a footprint in the country. Many of these players are active in the reinsurance business. However, unlike the DIFC-based companies, entities based within QFC are permitted to seek direct insurance business throughout Qatar. Insurance companies operating out of QFC continue to be independently regulated by the Qatar Financial Centre Authority, outside the purview of Qatar Central Bank.

By permitting 100 percent foreign ownership and imposing no currency restrictions, the QFC has become an ideal destination for companies looking to establish their presence in the expanding GCC insurance industry. The QFC has significantly contributed to the growth of the regional insurance industry and is home to a number of insurance, reinsurance and insurance intermediaries.

Qatar Financial Centre

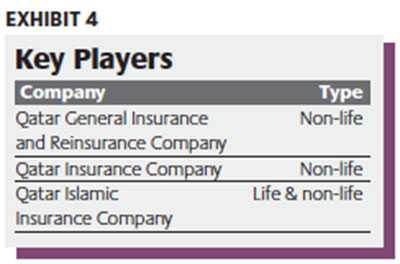

For example, global giants such as AXA, Marsh and Zurich operate alongside major domestic companies including Q-Re, SEIB Insurance and Reinsurance, Qatar General Insurance and Reinsurance and Qatar Islamic Insurance.

QFC has paved the way for bringing international expertise and best practices into the regional market and has contributed immensely to the structural progress of the industry.

Main lines of business:

Energy, marine and construction are the major lines of insurance in Qatar given its robust hydrocarbons sector and are likely to remain prominent in the foreseeable future.

Compulsory lines of business:

Needless to say, third- party motor insurance is compulsory and the segment accounts for a large portion of the personal non-life insurance market. It is the most competitive business line, generating low margins for the service providers.

Currently, health insurance does not constitute a large slice of the industry as it does in some of the other GCC markets. Government benefits through provision of free and subsidised healthcare for nationals and expatriates have curtailed growth of this segment.

Nevertheless, with the Supreme Council of Health expected to implement a compulsory medical insurance program for all nationals, expatriates and visitors in Qatar starting 2014, the health insurance segment is likely to see a higher industry representation in the future.

Life:

The life insurance segment remains highly underdeveloped and the principal market for conventional life products is still the large composition of expatriate residents in Qatar.

Other personal lines of insurance like property have also experienced a slow progress due to high social spending and influence of cultural beliefs.

Key players:

Qatar’s insurance industry consists of relatively fewer players than the other GCC countries, thus making the market more concentrated particularly at the top. Currently, there are 27 licensed insurance and reinsurance companies in the country.

Government sponsored projects are mainly covered by domestic companies. Subsequently, the market is largely controlled by these companies, with Qatar

Retention levels:

Given the majority contribution of commercial lines in the overall insurance premium and lack of necessary expertise, the primary insurance players in Qatar rely heavily on reinsurance companies to cover risks.

Recent Industry developments:

In May 2013, the insurance industry in Qatar was forecast to expand by over five percent year-on-year in 2013 and outperform most of the other GCC markets. Robust infrastructure spending in the country was seen as one of the major growth drivers.

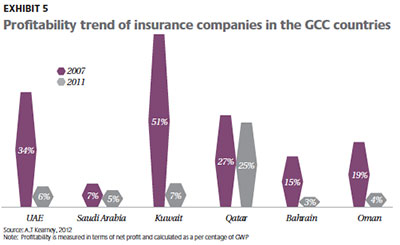

Qatari insurance companies experienced a 25.5 percent year-on-year increase in net profit in the first quarter of 2013. The profit growth of most of the companies was substantially better than that in the same period of last year.

In March 2013, the chief executive of Lusail Real Estate Development Company stated that the number of insurable assets is likely to increase at a high rate in Qatar with several mega projects being planned in preparation of the 2022 FIFA World Cup, which sets the stage for increasing awareness towards insurance and risk management practices.

Most of the insurance companies either cede their entire premium or retain less than 10 percent of the risk. The country has one of the highest cession rates in the region and large international companies have emerged as key players in the reinsurance market. Motor and medical insurance are the two businesses retained to the highest extent in Qatar. Qatar has a relatively low retention rate given the high share of premium coming from high-risk engineering, energy and other commercial projects.

Nevertheless, over the years, retention rates of primary insurers have increased due to change in product mix in favour of health insurance products and improvement in the level of expertise.

Distribution Channels:

Distribution of insurance products in Qatar is primarily through the direct channel and intermediaries account for approximately 25 percent of total premium written, especially in the personal business lines. The use of bancassurance as a distribution medium has so far been low, but is gradually gaining momentum. Not only are insurance companies collaborating with banks for selling insurance products, but banks are also starting to use insurance companies as a sales medium. About 75 percent of market participants surveyed by the Qatar Financial Centre Authority in 2012 mentioned ‘bancassurance’ to be one of the fastest growing distribution channels in the GCC over the next couple of years.

In April 2013, Qatar National Bank was reported to be launching a new bancassurance product, which integrates a savings plan and insurance cover, to be distributed through MetLife Alico.

Valuation of Qatari insurance market:

QFC offers a regulatory, operating and tax framework, which makes it appealing as a market to foreign investors. The multiple of Qatar-based insurance companies was higher than the regional average reflecting high potential growth of these companies, as perceived by investors.

Challenges:

1. Intensive Competition:

Most of the market participants who were part of the survey by the Qatar Financial Centre Authority in 2012 did not foresee a market consolidation over the coming 12-24 months.

2. Inadequate Regulation:

In the State of Qatar, two different sets of regulations co-exist, one within the financial centre and the other applicable to domestic market outside the financial centre.

|