We are well versed with the idiom, “Make hay while the sun shines”. But how many of us have really put it into practice? ta’ameen Qatar talks to Carlton Crabbe, Partner at AES International Qatar to know how to plan, protect and grow wealth for the golden phase of one’s life….Retirement.

Introduction:

Qatar’s strong and stable economic growth over the last decade has led it to be ranked in the world’s top fifty countries for gross domestic production. This is a staggering feat compared to Western economies, which have struggled to register positive growth every year since the financial collapse of 2007.

With Qatar’s background of virtually uninterrupted economic growth and a healthy economy, one of the last considerations of expatriates living and working in the richest nation on the planet (per capita) is planning for retirement. But one day, most expatriates will inevitably return home, or retire to another country. Planning for this day can often be daunting because we can never be sure what the future would look like. With the quality of life in Qatar being very high and expatriates enjoying many benefits of living in the country, such as tax free salaries, affordable domestic help and high quality healthcare (to name a few), it is important not to bury one’s head in the sand when it comes to retirement planning.

Carlton Crabbe, Partner, AES International Qatar

Planning Today, For A Better Tomorrow:

Planning for tomorrow must start today if expatriates hope to maintain a good lifestyle into their retirement. Pension plans, regular savings plans and residential property are the most common forms of retirement savings among expats and all these asset classes have their place and a part to play in providing for our twilight years. However, retirement planning should start with a solid foundation and this is where financial planning, with the help of a professional adviser using lifetime cash flow modelling, can help.

The starting point for a conversation between a financial planner and a client is not a financial product, but is a holistic conversation starting with how you spend your current income. A review of your bank statements and credit card bills will quickly reveal how you live and where your financial resources are spent.

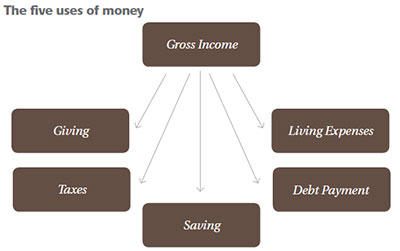

This can be broken down into the five areas pictured showing the choices you make with your income.

This exercise can be very revealing and helps clarify for client and financial adviser alike how a client is living and where their current priorities are. By looking at each category of spending, we will often be able to streamline our finances and reduce unnecessary spending and take those crucial first steps to financial freedom.

It is worth noting that The Five (5) Uses of Money table includes income taxes, which are not applicable to residents of Qatar, but we encourage clients to consider the impact of taxes on their retirement incomes when they return home. For example, wealthy Brits will typically pay 45 percent top rate of income tax, the French 45 percent and some Americans over 50 percent.

Once you have completed your expenditure and budget review, the next step is to discuss with your financial planner your goals, your ambitions and your dreams. Most people’s goals include one or more of the following areas: family, career, health, friends and travel.

Pension plans, regular savings plans and residential property are the most common forms of retirement savings among expats.

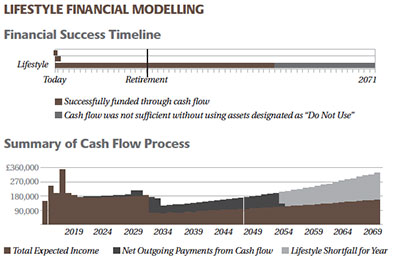

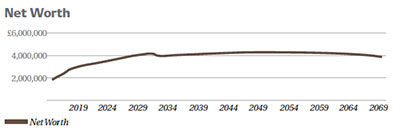

Your financial planner will then be able to help you calculate the financial cost of each goal and put each of your goals into a lifetime cash flow planning model, which will show your (client’s) existing assets, income, debts and future growth in easy-to-understand graphs.

The benefit of lifestyle financial modelling is that it helps to clearly see what may happen in the future under different financial return scenarios. It is important to remember that your financial life will not necessarily turn out like this, but nevertheless, it allows us to help you plot a financial course with much more certainty than before. Your saving will take on a greater purpose and your goals will become achievable or realistic because you have taken the time to plan and focus on how to achieve them.

Most importantly, a good financial planner wants you to have the financial freedom that you will experience when you take the time to plan for your retirement and other life goals.

Financial advisers often talk about risk in terms of investments. Whilst this is important and forms part of our advice on how to invest your money, at AES International, we start by looking at risks differently.

“Life is full of risks and, whether you like it or not, the financial planner’s job is to minimise them. Risk is not the volatility of the investment markets; it is the failure to achieve our client’s objectives.”

The risk that you may not be able to retire at, for example, 60 years old, is very real for many expatriates. ‘Have I got enough?’ is the question our clients ask us time and time again. In other cases, it is ‘I know I have enough, but what can I do to provide for my children and grandchildren?’ These are deeply important questions to many of us and once we have established our client’s needs, we can complete the lifetime cash flow modelling which gives us the rate you will need to grow your assets by each year in different scenarios to achieve your goals. There are typically four outcomes after you have completed the financial modelling with your planner.

Positive:

1. You will be able to meet your goals if you stick to your budget and savings plan and take no investment risk.

Negative:

2. You will not be able to achieve your goals given your current budget and level of savings, so you will need to save more.

3. You will not be able to save any more. Therefore, you will need to invest the savings you are making each month or year and this involves taking investment risk with your money.

4. You do not wish to take investment risks with your money and you cannot commit to saving any more. In this case, you will need to re-visit your plans and work through a more achievable set of goals.

As a client, you will now be in a good position to understand if committing to those goals is attainable and realistic. If you believe they are, you then need to commit to them with your adviser in order for you to reach them. Financial planning is not just about picking investments. It is about developing emotional discipline and setting realistic expectations about what you can achieve, and in this case, when you can retire.

Once this is done, it is time to talk about investment risk and your tolerance to it. Too little tolerance, or risk aversion, can prevent us from achieving some of our dreams, whether it be financial independence or early retirement. Too much tolerance to risk, or risk taking, can cause unpleasant financial surprises, which means we also miss our aspirations.

All professional financial planners will ask a client to complete a personal financial risk profiling questionnaire. By answering a series of questions on risk and how you would view certain scenarios, the risk questionnaire provides the starting point to discuss risk in more detail and your tolerance to it with your adviser. The actual level of risk you need to take will be defined by your objectives and goals.

When it comes to investing, a professional adviser will rely not on his

or own top fund picks of the day, but on a qualified, experienced investment professional, like a discretionary fund manager, to build a bespoke portfolio. This portfolio should balance the risks and rewards you have expressed in your risk profiling exercise with your individual goals that you have discussed in your lifetime cash flow modelling.

The investment portfolio will typically be made up of equities, bonds and government debt, with some portfolios holding other assets like private equity, hedge funds and currency. This is known as your asset allocation, which is the optimum combination of investments needed in order to give you the potential to meet the goals you set with your adviser.

However, if the proposed portfolio is too risky for your tolerance, you will need to revisit the four outcomes from your lifetime financial modelling and decide whether or not you are prepared to compromise on your goals or if you are willing to take on more risk to achieve them.

Remember, risk will change over time, and if you are nearing retirement, you and your financial planner should monitor your investments at each review meeting and if necessary, start to reduce the investment risk you are taking in order to make sure you remain on track to meet your desired retirement date.

Sometimes, your finances will be ahead of schedule and sometimes they may be behind, but most importantly, as a client, you must commit to your goals, emotionally and financially. Financial planners need to commit to a long-term client relationship, take clients through lifetime cash flow modelling, make sure they have fully understood their clients’ goals and dreams and have recommended a suitable investment portfolio, which they then review regularly against the benchmarks that have been set. A great financial adviser can make a difference to whether or not you retire on time with your hopes.

|