ta’ameen Qatar summarises S&P’s report and casts a spotlight on Qatar’s risk aggregate and depicts how banks are now a promising conduit for spreading the need and purpose for insurance in the State of Qatar.

Qatar’s strong net external and fiscal asset positions balance the concentration risk related to the economy’s reliance on the oil and gas sector. Standard & Poor’s affirmed its long and short-term foreign and local currency sovereign credit ratings of the State of Qatar at ‘AA/A-1+’, stating that the outlook is stable.

Ratings outlook:

Qatar’s ratings are a reflection of its economic wealth and strong fiscal and external balance sheets. The ratings are constrained by limited monetary policy flexibility, nascent public institutions and limited disclosure, particularly with respect to government assets and investment income.

According to S&P’s credit analyst Trevor Cullinan, “Qatar is one of the wealthiest economies we rate, with GDP per capita estimated at USD 94,000 in 2013. We estimate ‘trend’ growth, which we define as a weighted 10-year average of real GDP per capita growth, at around -0.3 percent”.

In S&P’s view, Qatar's high wealth levels mean that its relatively weak economic growth performance is not an immediate concern for ratings. However, over the medium term, Qatar's economic risk position could deteriorate relative to faster-growing economies.

It is expected that the national development strategy projects will improve the economy’s productive capacity and strengthen Qatar’s competitive position.

The stable outlook balances S&P’s view of Qatar's high economic wealth levels and strong external and fiscal positions against its institutional shortcomings and limited monetary flexibility.

Calculating risk scores:

Standard & Poor’s bank criteria use its BICRA economic risk and industry risk scores to determine a bank’s anchor, which is the starting point in assigning an issuer credit rating. The anchor for banks operating in Qatar is ‘bbb’.

Banks’ risk appetite:

Qatar has made some progress towards diversifying its economy although it still depends heavily on oil and Liquefied Natural Gas (LNG) production. It is believed that the economy will continue to show strong, although slowing momentum, reflecting Qatar’s robust private consumption and significant infrastructure development program.

Qatar’s commercial sector still remains more vulnerable to risks than the housing segment. This is one of the main risks faced by the Qatari banking sector, given its high concentration in lending to cyclical sectors like real estate and construction.

Though Qatari banks’ risk appetite remains high, the lending growth is expected to decelerate to about 15 percent in 2013 and in the years ahead. Moreover, growth will be driven to a large extent by exposure to the government, government-related entities and a handful of major local groups involved in government-backed projects, where the risks are more limited.

Qatar’s political risk weighs on S&P’s assessment of Qatar’s economic resilience, as the country faces geopolitical risk. Moderating lending growth over the next few years is expected. Qatar’s Central Bank is currently tightening regulation, which may further limit business and lending growth in the short to medium term.

The trend for industry risk in the Qatari banking sector is stable. The Qatari banking industry has an adequate share of core deposits, strong efficiency and increasingly stringent lending practices. However, risk appetite remains elevated with high exposure to real estate lending and ambitious expansion abroad.

The Qatar Investment Authority (QIA), Qatar’s sovereign wealth fund, bought another 10 percent stake in domestic banks in the first quarter of 2011, in an effort to increase their capital bases, following similar moves in 2009-2010. This capital injection was intended to strengthen banks’ balance sheets in view of Basel III requirements and to enable them to fund higher loan growth ahead of the 2022 FIFA World Cup.

Banks: Leading to increased insurance uptake:

The fast pace of growth experienced by Qatari banks is due to strong support provided by the Qatari government. Not only that, but an increasing demand for domestic credit owing to a large number of infrastructure projects is further fueling this stupendous growth.

Credit analyst Timucin Engin believes that this may eventually lead the Islamic banks to look at overseas expansion.

The government of Qatar intends to make the country a centre for Islamic banking and so far, its strategy has been succeeding. Qatar now has one of the fastest-growing Islamic banking sectors in the world, thanks to a surge in the demand for local credit to finance government infrastructure and investment projects.

Timucin Engin

It is believed that this demand will endure and that the assets of Qatar’s Islamic banks will continue to grow. Needless to say, the country's banking system will continue to rise and create more channels for distribution of insurance products.

Sustainability:

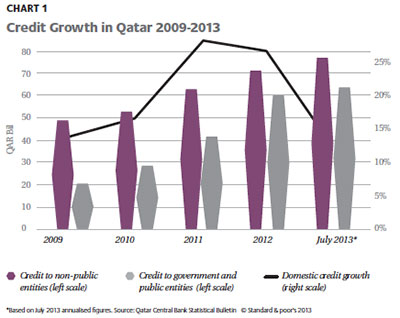

Once the infrastructure projects slow down, sustainability of growth of Qatari banks over the long run remains questionable particularly because Qatar has a very small bankable population. Moreover, Qatar’s debt capital markets are at a nascent stage and the bulk of its credit generation derives from bank lending. It is therefore on account of the Qatari government’s large infrastructure and investment projects that the country’s domestic credit grew at a compound average rate of 30.9 percent between 2006 and 2012.

Albeit a visible slowdown in lending was observed in the first half of 2013 due to administrative delays with certain projects, credit growth is expected to reaccelerate in 2014, when major infrastructure projects start in preparation for Qatar hosting the 2022 FIFA World Cup. This in turn will bolster the domestic demand for credit in the country and support the lending activities of Islamic banks and open the market for short term financing and credit insurance.

Futuristic outlook:

The total balance sheet of Qatar’s Islamic banks was USD 54 billion as of year-end 2012. Assuming that the banks grow by an average of 15 percent over the next five years – which is significantly lower than the previous five-year average of 35 percent, we could see the Islamic banks’ asset base exceeding USD 100 billion by 2017. This could indeed place Qatar’s Islamic banking market as the third-largest in the Gulf region, after Saudi Arabia and the United Arab Emirates.

A ‘growing’ Islamic banking centre:

The Qatari government’s strategy to grow Qatar as an Islamic banking centre clearly shows that it is highly supportive of this sector. Further, as an Islamic country, Qatar is committed to the principles of Sharia. Islamic banks currently represent one-quarter of Qatar’s banking system in terms of assets, up from 13 percent in 2006 and it is anticipated that they will continue to gain market share.

For example, in 2011, Qatar Central Bank (QCB) banned conventional banks from extending Islamic banking products through ‘Islamic windows’ in the onshore conventional banking system, thereby requiring conventional banks to close or divest their Sharia-compliant businesses and not underwrite any new Sharia-compliant loans. As a result, Sharia-compliant banking shifted to the Islamic banks. There are currently four Islamic banks in Qatar, with a combined asset base of USD 54.4 billion as of end-June 2013.

The total asset base of the Qatari banking system reached over USD 240 billion as of July 31, 2013, and the government's planned infrastructure projects give enough reason to believe that the banking system will continue to grow at a fast pace for several more years.

However, the total population of Qatar is less than two million and expatriates and foreign workers represent a predominant portion of this figure. In addition, the latter group tends to have relatively limited assets in the Qatari banking system. Therefore, Qatar's bankable population, as in many other GCC countries, is limited. Consequently, one of the major concerns about the Qatari banking system is whether the pace of growth will slow once the number of government projects falls in future.

Effects of Basel III Regulation:

Historically, Islamic banks have not been very active in the debt capital markets, with only Qatar Islamic Bank and Qatar International Islamic having issued sukuk.

In addition, the contractual maturity of the deposits collected by the Islamic banks is very short term, whereas the lending tenors are substantially longer.

However, it is believed that funding and liquidity requirements of the incoming Basel III regulatory standard will move the Qatari Islamic banks to tap the debt capital markets more actively over the next few years and raise longer-term funding.

Summary:

The outlook for both the Qatari banking system and its Islamic banks are expected to be stable over the next two years. The Qatari government's large infrastructure investments and its highly supportive stance during the global financial crisis of 2008-2009 have enabled the Qatari Islamic banks to benefit from fast-paced credit growth and report strong margins and low credit losses. This has aided in opening the Qatari market and spreading awareness about personal insurance products and business insurance.

|