Qatar’s National Vision 2030 sets out the Qatari government’s goal of improving health of Qatar’s population by developing a world class and integrated healthcare system. Wayne Jones, Partner and Ramiz Shlah, Associate at Clyde & Co present an update on the National Health Insurance Scheme, which would be accessible to all citizens, residents and visitors and is in the process of being implemented in five phases.

Ramiz Shlah, Associate, Clyde & Co

Wayne Jones, Partner, Clyde & Co

As the population of Qatar is expected to rise to four million by the end of the decade, the Government of Qatar has indicated that expanding health coverage in Qatar is necessary to achieve the following fundamental pillars of the Health Insurance Scheme:

Giving access to first-class healthcare to the entire population

Increasing the quality and range of healthcare

Increasing competition amongst private healthcare providers thereby increasing choices available to patients.

The Health Insurance Scheme was enacted through issuance of Law No 7 of 2013 concerning the Social Health Insurance Scheme (the Health Insurance Law). The Health Insurance Law was published in the Official Gazette – Issue No. 10 dated 16 June 2013. Pursuant to Article 29 of the Health Insurance Law, the Minister of Public Health and secretary general of the Supreme Council of Health (SCH) is tasked with issuing “Executive Regulations”. Executive Regulations have been issued pursuant to Resolution No 22 of 2013 of the Minister of Public Health issuing the implementing Regulations for Law No 7 of 2013 concerning the Social Health Insurance Scheme (the Executive Regulations) in the Official Gazette – Issue No. 16 dated 28 October 2013. The Health Insurance Scheme envisages a package of prescribed basic healthcare services requiring mandatory insurance cover, which will fall under the SCH’s regulatory mandate.

Article 5 of the Health Insurance Law tasks the SCH with the responsibility, supervision and development of the Health Insurance Scheme. Separately, Article 19 of the Health Insurance Law tasks the National Health Insurance Company (NHIC) with the “actual implementation and management” of the Health Insurance Scheme. The NHIC is a fully owned government entity with a board of directors formed of representatives of the SCH, Ministry of Finance, Ministry of Labour, Ministry of Interior, Central Municipality Council and two members from the private business sector. The NHIC’s powers are set out in more detail in Article 20 of the Health Insurance Law and the Executive Regulations.

The NHIC has appointed Al Khaleej Takaful as its third party administrator to handle essential administrative processes and support building its capabilities. Aetna and GlobeMed have been appointed as exclusive subcontractors of the third party administrator. Aetna will provide the NHIC with a range of health management services, including clinical management and disease management. GlobeMed will manage enrollment, claims administration and the NHIC’s call centre capabilities, among other functions.

The SCH has indicated that expatriates (non-national residents) will be enrolled in the Health Insurance Scheme upon renewal of their residence permits by payment of a premium, which is to be covered by their employer or sponsor.

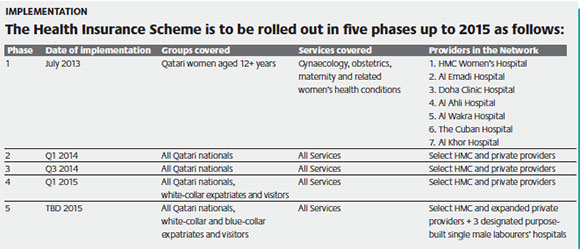

Beneficiaries of the Health Insurance Scheme will be able to obtain services from both public and private healthcare providers. Currently the following seven healthcare providers are participating in the Health Insurance Scheme:

HMC Women’s Hospital

Al Emadi Hospital

Doha Clinic Hospital

Al Ahli Hospital

Al Wakra Hospital

The Cuban Hospital

Al Khor Hospital

The SCH has indicated that nearly 5,000 Qatari women have made use of the Health Insurance Scheme as of July 2013. As each new category of beneficiaries is eligible to enter the scheme, presentation of one's Qatari ID card will suffice to allow citizens and residents to obtain healthcare services.

Executive Regulations:

The Executive Regulations contain a number of conditions which impact the operation of the Health Insurance Scheme and its participants. Article 16 of the Executive Regulations provides that a health insurance provider’s place of business must be inside Qatar and that it shall be licenced by the competent governmental authority in Qatar.

Further, Article 16 provides that health insurance providers “shall not manage or run, either solely or jointly, any healthcare services rendered to the beneficiaries inside the State.” The relationship between health insurance providers and healthcare providers will have to be managed appropriately by the SCH and market participants.

Amongst other things, the Executive Regulations also include various articles concerning patient confidentiality, including the principle of “patient-doctor confidentiality”. The disclosure of patient files is prohibited in Article 27 of the Executive Regulations except in specific circumstances required for the operation of the Health Insurance Scheme or pursuant to government action.

Article 32 of the Executive Regulations also introduces a complaint and grievance submission procedure for "[a]ny person who is harmed as a result of the violation of the Law and these Regulations.” Interestingly, the Executive Regulations permits complaints to be submitted in Arabic or English.

Premiums:

Article 13 of the Health Insurance Law provides that the Government of Qatar shall be responsible for paying health insurance premiums for Qatari nationals. It would also appear likely that the Government of Qatar will cover health insurance premiums of GCC nationals, although there is no explicit article mandating such in the law.

Health Insurance Law provides that the Government of Qatar shall be responsible for paying health insurance premiums for Qatari nationals.

Stakeholders will also be interested to know that employers and sponsors are responsible for paying health insurance premiums for their employees (and their families) and sponsored persons respectively. Visitors are responsible for paying their own health insurance premiums for the duration of their stay in the country, which will be payable prior to issuance or renewal of a visa pursuant to Article 15.

Article 18 prohibits employers and sponsors from recovering any health insurance premiums from employees (and their families) or sponsored persons. Employers and sponsors are eagerly awaiting further guidance on the amount of health insurance premiums payable under the Health Insurance Scheme.

The amount of health insurance premiums shall be based on “generally accepted actuarial principles” to be paid in accordance with the ratios and measure prescribed in the Executive Regulations pursuant to Article 12 of the Health Insurance Law. The SCH is responsible for setting the amount of health insurance premiums according to Article 14. The Executive Regulations do not set out the amounts of any health insurance premiums for basic healthcare services or any tariffs that might apply to additional healthcare services. Nor do the Executive Regulations provide any indication as to whether there will be any mandatory premiums applicable to, for example, lower income residents.

Article 2 of the Executive Regulations provides that health insurance premiums shall be set without discrimination between beneficiaries in respect of age, gender, previous health status or any other risk factors. Article 2 goes on to provide that “The premiums shall be paid as a percentage of all costs of the healthcare activities, in addition to the actuarial forecasts and modeling set by the Council, provided that such premiums shall not include profits.” The interpretation and application of the foregoing article will influence the amount of health insurance premiums payable by the Qatari government, employers and sponsors.

There will also be a period between the launch of Phase 1 and Phase 4 whereby the Health Insurance Scheme will work concurrently with private health insurance. The SCH has indicated that: “This period is designed to allow employers the time to reconcile the coverage of employees between their existing health insurance plans and the National Health Insurance scheme. By removing the elements of double coverage, they [employers] can recover the portion of fees paid for their existing plans.” The mechanism by which the SCH will seek to protect employers and sponsors from paying for both private and public health insurance policies during the roll out phases of the Health Insurance Scheme, and the manner in which double insurance will be avoided are yet to be defined.

In order to avoid potential price increases of healthcare services, the SCH has instituted a moratorium on price increases for healthcare services offered by private healthcare providers until the Health Insurance Scheme is fully implemented. According to the SCH Circular No 7 of 2013, the SCH has indicated that “All private healthcare facilities in Qatar should comply with the price list approved by the department of healthcare quality and patient safety. Furthermore, the department will not accept any price increase requests for health services provided by all health institutions in the country until the completion of the application of the heath insurance system. The only exception to this decision would be by adding new medical services after getting the approvals required by the department.”

Basic & Additional healthcare services:

Article 1 of the Health Insurance Law distinguishes between “Basic Healthcare Services” and “Additional Healthcare Services”. Basic Healthcare Services are defined as “A range of healthcare services, which shall be provided to the beneficiaries in accordance with the provisions of this Law.” Additional Healthcare Services are defined as “A range of healthcare services, which may be provided in addition to the basic healthcare services to the beneficiaries in accordance with the provisions of this Law.”

Insurance cover for basic healthcare services will be mandatory for all Qatari nationals, GCC nationals, residents and visitors pursuant to Article 2 of the Health Insurance Law.

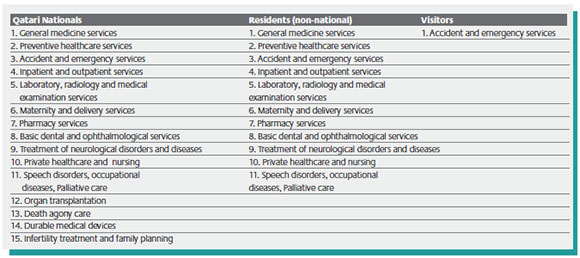

According to the Executive Regulations, basic healthcare services include following preventative, therapeutic and rehabilitative services and medical tests.

Under the law it appears that mandatory insurance cover for all basic healthcare services will be provided by NHIC alone. Accredited health insurance companies will be entitled to offer insurance cover for additional healthcare services only (i.e. the private insurance market will not be entitled to offer cover for basic healthcare services).

In order to participate in the Health Insurance Scheme, healthcare providers will be required to obtain SCH approval in order to offer some or all of the basic healthcare services. The Executive Regulations, pursuant to Article 9, shall specify the conditions and controls for healthcare providers to subscribe to the Heath Insurance Scheme.

The general secretariat of the SCH is also tasked with making recommendations to the Minister and the SCH on the amount of co-payments which may be payable for basic healthcare services.

Article 10 indicates that employers and sponsors may provide their employees and sponsored persons with additional healthcare services through private medical insurance in accordance with the “controls” to be set forth in the Executive Regulations. Article 11 indicates that the SCH shall issue licences to health insurance providers to market and sell insurance policies in respect of additional healthcare services in accordance with the licencing conditions set for the Executive Regulations and the ones referenced above.

Comment:

The Health Insurance Scheme is a significant step put forward by the Qatari government to overhaul healthcare funding in Qatar. The system put forward by the Health Insurance Law and the Executive Regulations contemplates an employer-funded fee-for-service proposal, with the government bearing the costs for Qatari nationals.

|