The Qatari insurance market has grown at a steady rate in recent years and is expected to outpace most of its neighbours in the coming years. Sinchita Mukherjee takes a closer look at A.M. Best’s report on Qatar.

Sinchita Mukherjee, deputy editor, ta’ameen Qatar & Premium magazine

Unification of regulatory bodies:

Laws passed for creating a new regulatory regime and the unification of the insurance regulatory bodies will assist improved regulation and governance across the market, which may create a robust regulatory platform for insurance awareness and ultimately lead to growth.

Role of the QFC:

Since 2005, insurers have had the option to be licensed under the independently operated Qatar Financial Centre (QFC), which is considered to have one of the better-regulated regimes in the GCC. The QFC was established to create an onshore centre accessible to regional markets operating under the more robust Qatar Financial Centre Regulatory Authority (QFCRA). It conforms to sound regulatory practice and international standards.

Takaful window:

The QFCRA has also made specific provisions recognising Takaful as a separate type of insurance in its regulatory regime in the Prudential Insurance Rule-book (PINS). Rules for Takaful operators have also been set out by the QFCRA in the Islamic Finance Rulebook.

Market overview:

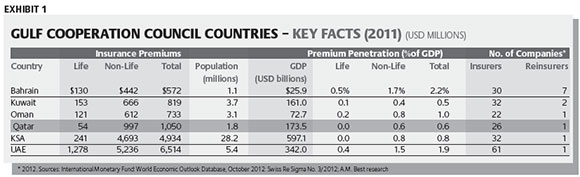

Insurance premium as a percentage of Gross Domestic Product (GDP) was one of the lowest in the GCC at just 0.6 percent highlighting both the potential and the challenges for growth of the Qatari insurance market (Exhibit 1).

Growth drivers:

Energy prices are currently above government forecasts, which enable infrastructure development and raise the demand for insurance. Furthermore, the Qatari government is continuing its capital spending on building infrastructure in an attempt to diversify the country’s economic base away from the energy sector.

Economy:

Qatar’s economy has experienced a very rapid growth over the past few years, with GDP increasing by 16.7 percent in 2010, 14.1 percent in 2011 and an estimated 6.3 percent in 2012. Economic growth is expected to moderate to 4.9 percent in 2013, although spending on infrastructure is anticipated to continue. Economic development is expected to rise further for hosting the 2022 FIFA World Cup.

Health insurance:

The proposed introduction of universal compulsory medical insurance by 2014 would provide another substantial boost to the market, though most of the growth is likely to be absorbed by a newly formed national health insurer.

The Supreme Council of Health (SCH) is introducing a national health insurance plan to be rolled out in stages by 2014. The proposed programme would initially include Qatari nationals, before being extended to the private sector, expatriates and tourists. The state would provide coverage for its citizens, with companies responsible for its expatriate staff.

Mandatory health insurance is expected to prompt significant growth for the young private health insurance sector. Compulsory healthcare coverage should provide opportunities to Qatari insurers, although a prudent underwriting approach will be needed to write this product profitably. Despite the limited number of companies offering healthcare products, underwriting can still be challenging given the increasing competition and high level of medical claims inflation.

Lines of business:

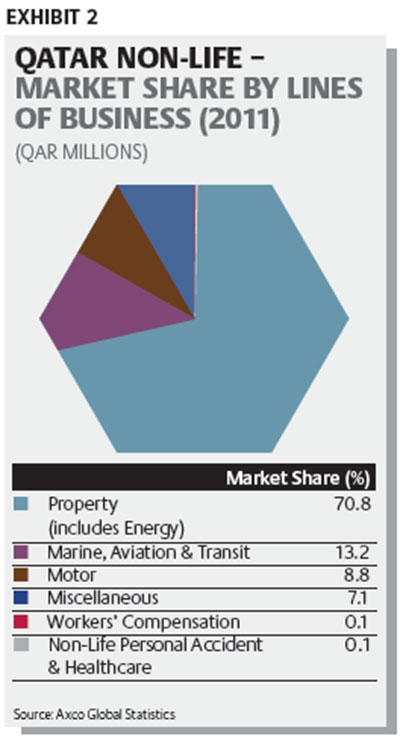

The insurance market is largely driven by non-life related risks. (Exhibit 2).

Commercial risks:

Commercial risks are heavily reinsured into the international market, with most direct writers either fronting this line or retaining less than 10 percent of premiums.

Motor:

On a net basis, the main line of business retained in Qatar is motor followed by medical. Tariffs for Motor Third Party Liability (MTPL) are set by the insurance regulator, which monitors market performance and adjusts rates accordingly. Profitability for MTPL tends to be at the borderline. Companies cross-subsidise with comprehensive products, which are priced in the open market.

However, it produces low margins compared to that of other business lines that benefit from material inward reinsurance commissions.

Energy & Construction:

Given Qatar’s insurance market is focused heavily on the energy and construction sectors, insurers must manage high value and volatile risks effectively. This leads to low retention levels and a dependence on international reinsurance markets for support, which can lead to significant levels of counterparty credit risk and potentially higher costs driven by international market forces.

Retention levels:

Retention levels have continued to increase, from approximately 35 percent in 2006 to more than 50 percent in 2011. Drivers for the increase in retention include a change in the business mix of many insurers stemming from the growth of medical business and companies gradually accepting greater responsibility for underwriting risks as they gain more expertise.

Challenges:

Qatar has seen a marked increase in participants following the establishment of the QFC as many regional and international companies have established a presence through subsidiaries or branches. In total, there are 26 insurers and one reinsurer licensed to operate in Qatar, compared to 20 entities in 2010.

Competition:

Although along with the opportunities, increased competition is expected, which may place greater pressure on companies’ technical performances. Insurers face the challenge of growing their franchises in a competitive environment while maintaining profitability. The capital strength of primary insurers remains robust. However, the ability to service these capital levels may be difficult.

The market is dominated by Qatar Insurance Company (QIC), which underwrites more than 50 percent of the premium in Qatar. More recently, QIC has expanded internationally through the formation of Q-Re, which has high ambitions to penetrate the international reinsurance market. In addition, there have been plans for Al Koot Insurance and Reinsurance Company – a former captive of Qatar Petroleum to become a reinsurer. In this environment, international players tend to focus on writing specific risks or lines of business and in particular, the larger commercial and energy risks.

Risk management:

The most important factor for many domestic insurers is their ability to effectively manage the accumulation and concentration of risks. It is important that companies understand their exposures and mitigate these risks effectively. Therefore, direct writers must ensure that a strong panel of reinsurers supports them in order to reduce counter party credit risk, particularly for facultative exposures that can be substantial.

Market realisation:

The performance of Qatar’s leading six insurers, which represent more than 80 percent of total premiums, shows that the market and companies are profitable. The analysis is based on the annual reports of QIC, Qatar General Insurance and Reinsurance Company, Al Koot, Doha Insurance Company, Al Khaleej Takaful Group and Qatar Islamic Insurance Company.

The data that examines domestic business only, show the market’s estimated combined ratio has increased consistently in recent years, but remained at very profitable levels below 84 percent from 2006 to 2011. This is not an indication of reduced competition or have better underwriting performance in the market. It is a direct result of the high cessions of energy and commercial risks and the impact of reinsurance commissions, which result in depressing companies’ expense ratios.

Underwriting:

The rise in the estimated market combined ratio from 78 percent in 2006, to 84 percent in 2011, reflect largely increased expenses and higher acquisition costs. There has been an increase in medical business and a rise in the proportion of retained business. Despite increased competition, the leading insurers’ loss ratio remained below 70 percent during the six-year period, showing marginal improvement in the past few years. It fell from 70 percent in 2006 to 62 percent in 2011, which illustrates the market’s prudent approach towards underwriting.

Proportional to Non- Proportional business:

Expenses increased to 26 percent by 2011, from 16 percent in 2006, although these were offset by negative acquisition costs reflecting the high inward reinsurance commissions and relatively low commission expenses due to direct business. Acquisition costs deteriorated marginally in 2011. Reinsurers have reduced commission payments and introduced sliding scale commissions related to profitability. They also have offered less favourable commissions across the GCC in recent years, resulting in a general movement towards higher retention levels for local companies. In addition, there has been a gradual shift from proportional to non-proportional business, which changes the business mix and reduces overall commission costs for reinsurers, encouraging higher retention levels for local participants.

Investment yields:

While Qatar’s investment markets have suffered less than its GCC counterparts, investment income has been restricted in recent years by the depressed equity, real estate markets and low interest rates. Insurers face a prolonged period of low investment yields, which may make it difficult for some Qatari insurers to achieve their return-on-equity targets and will reinforce the need to focus on prudent underwriting.

ERM:

Enterprise risk management (ERM) frameworks for some companies have evolved over the years. While this shift is in the right direction, insurers need to continue developing internal ERM capabilities and processes, in particular with reference to capital management. Compared to international peers, ERM in Qatar requires further development.

|