The current scenario of falling oil prices may have an impact on the insurance industry, comments A.M. Best. A ta’ameen Qatar report.

The Middle East insurance markets have seen remarkable growth in premium revenue over the past decade. This growth has stemmed from the infrastructure and industrial opportunities arising from higher oil revenues, and through the introduction of mandatory insurance covers such as medical healthcare.

At present, insurance penetration rates remain lowest among emerging markets, and the introduction of compulsory insurance has bolstered insurance revenues in recent years.

Despite the recent fall in oil prices and the forecasted lower economic growth, most insurers rated by A.M. Best that are domiciled in the Middle East are adequately capitalised and well positioned to absorb the impact that lower oil prices will have on the insurance sector, including lower than expected growth in gross premium written and greater fluctuations inasset prices over the short term.

However, if oil prices were to remain low or below the Gulf Cooperation Council (GCC) countries’ budgets for a prolonged period, or if these countries were to show a contraction in economic activity, then the operating environment could prove challenging for the insurance market. Excess capital, fierce competition and lack of market discipline may place greater pressure on rates as insurers seek to expand their profiles within their core markets to produce a suitable return on shareholders’ capital.

High oil prices have previously dictated the high level of government spending on infrastructure, particularly within the GCC, as well as the level of investment activity from oil-rich countries into the wider Middle East region. As a result, these economies are highly reactive to changes in oil prices.

In recent years, Middle Eastern economies have boomed on the back of oil revenues. However, over the past few months, oil prices have declined to a five-year low as a result of lowered forecasts for demand from the sluggish global economy, higher supply from oil producers and an increase in US shale output.

On Dec. 10, 2014, the Organisation of the Petroleum Exporting Countries (OPEC) revised downward its prediction for world oil demand in its Monthly Oil Market Report, mainly due to lower than expected consumption in the Organisation for Economic Co‑operation and Development (OECD) region.

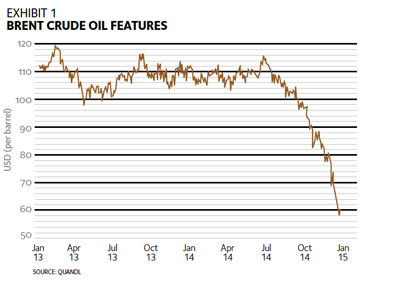

The price of Brent Crude subsequently fell to less than USD 60 per barrel – its lowest level since July 2009 (see Exhibit 1). A.M. Best believes anticipated lower forecasts for oil demand may translate into a slowdown in the insurance sector’s growth in the Middle East, as high oil prices have funded growth of gross domestic product (GDP) in the region. Many countries are attempting to diversify their income streams by promoting other sectors, notably tourism and financial services and, to a lesser extent, manufacturing. However, oil remains the most significant contributor to Middle Eastern economic development.

The ratings agency expects lower oil revenues to translate into lower growth in GDP, which may reduce economic stability and increase uncertainty in the region. This may have a direct impact on the regional dynamics of the GCC, where there is a high expatriate population; with employment within the Middle East becoming less attractive, expatriates may return to their home countries.

This could be a major concern for primary insurers, resulting in a possible contraction in the core personal lines of motor and medical. Primary insurers’ profiles are heavily weighted toward these lines of business on a net basis.

Coupled with this, reduced volumes of infrastructure projects may reduce the generous inward reinsurance commission primary insurers receive from large commercial risks, as this business largely tends to be ceded into the international reinsurance market. This potential change in insurers’ profiles could be further magnified as they balance higher expenses against declining business profiles.

Some countries are likely to find the current environment of low oil prices more difficult to operate in than others. Several GCC countries – in particular Saudi Arabia, Kuwait and the Emirate of Abu Dhabi – have built significant buffers to absorb the current reduction in oil prices, with spending on infrastructure projects likely to continue. In the short term, lower oil prices are unlikely to have a major impact on these governments’ expenditure programmes.

However, economies such as those in Oman and Bahrain depend more on high oil prices to sustain their current levels of economic development and to balance their budgets. Insurers operating within these two markets will face a greater challenge to maintain their business profiles over their GCC neighbours.

In the short term, there may be more concern over insurers’ investment strategies, given that many companies still have high exposure to equity and real estate assets within the GCC. The fall in the price of oil has had repercussions on investment markets, with GCC stock indices showing a substantial drop in recent weeks and a material slowdown in the appreciation of real estate assets. A.M. Best remains concerned over the aggressive investment strategies many insurers adopt in the region. While most insurers have sufficient capital to absorb the higher exposure to equity and real estate assets, fluctuating asset prices will create greater volatility in both operating performance and balance sheet strength.

Qatar, meanwhile, is positioned more uniquely, with its economy depending more on revenue from liquefied natural gas as opposed to that from oil production. Despite the influx of new insurance participants in Qatar, the market is less fragmented, with leading national companies enjoying competitive advantages and the country likely to benefit from major events such as the FIFA World Cup in 2022 and the country’s long-term economic programme, Qatar Vision 2030. Furthermore, impetus for the insurance market within the GCC will continue to be driven by the introduction of mandatory covers, as well as other events such as EXPO 2020 in Dubai.

As the majority of rated (re)insurers in the GCC currently are well capitalised and able to withstand a slowdown in insurance demand as a result of reduced government expenditure, A.M. Best is unlikely to take any rating actions tied directly to falling oil prices. To an extent, any reduced spending on infrastructure may be offset in part by the continued introduction of mandatory covers. Even in the case of economic contraction, A.M. Best believes there is still opportunity for increased insurance demand in the region, given the low insurance penetration in these markets.

|